.svg)

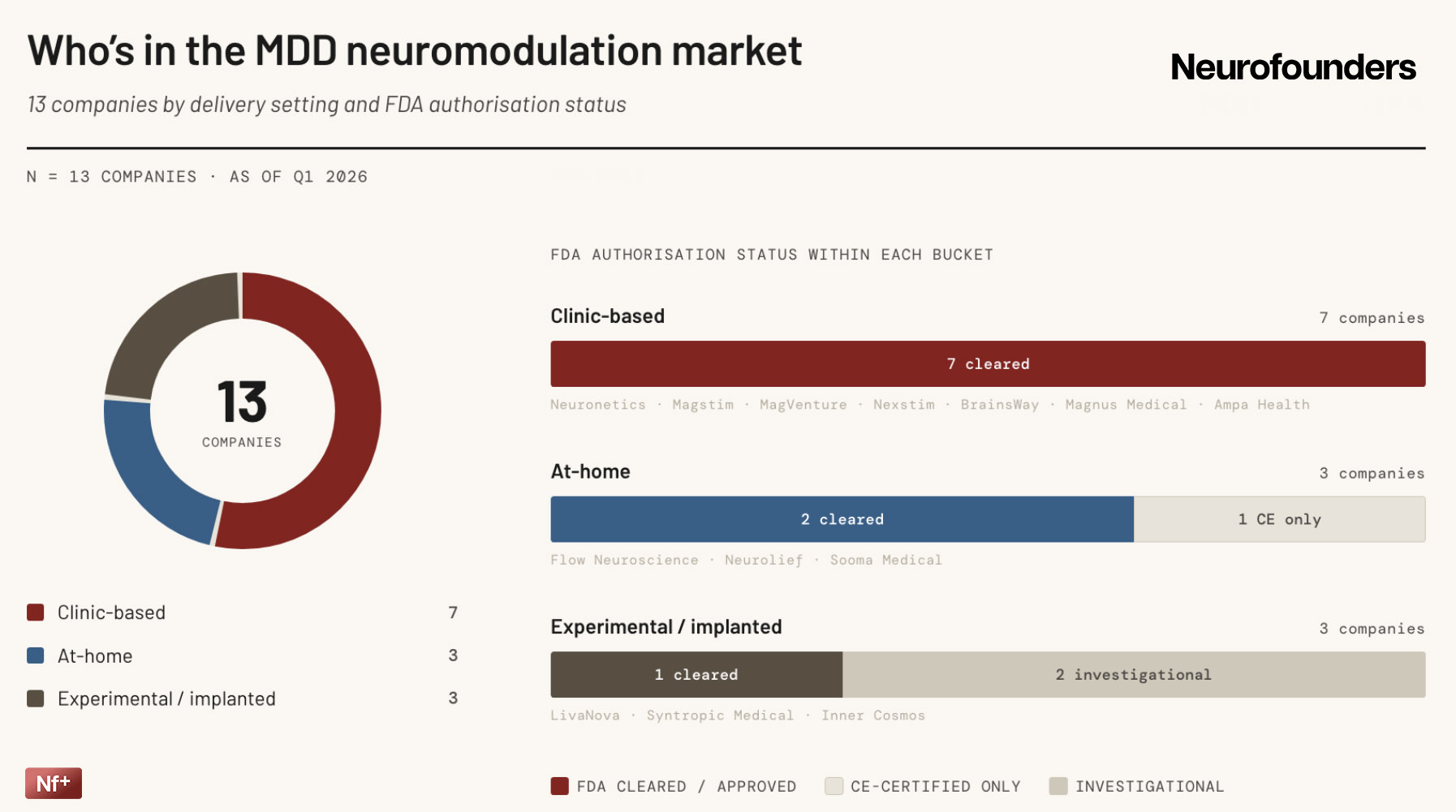

Neuromodulation in depression is moving into a new commercial phase. Neurofounders analyzed a focused snapshot of incumbent TMS platforms, newer protocol-driven companies, home-use devices, and a small set of early alternative approaches to see where that shift is showing up most clearly.

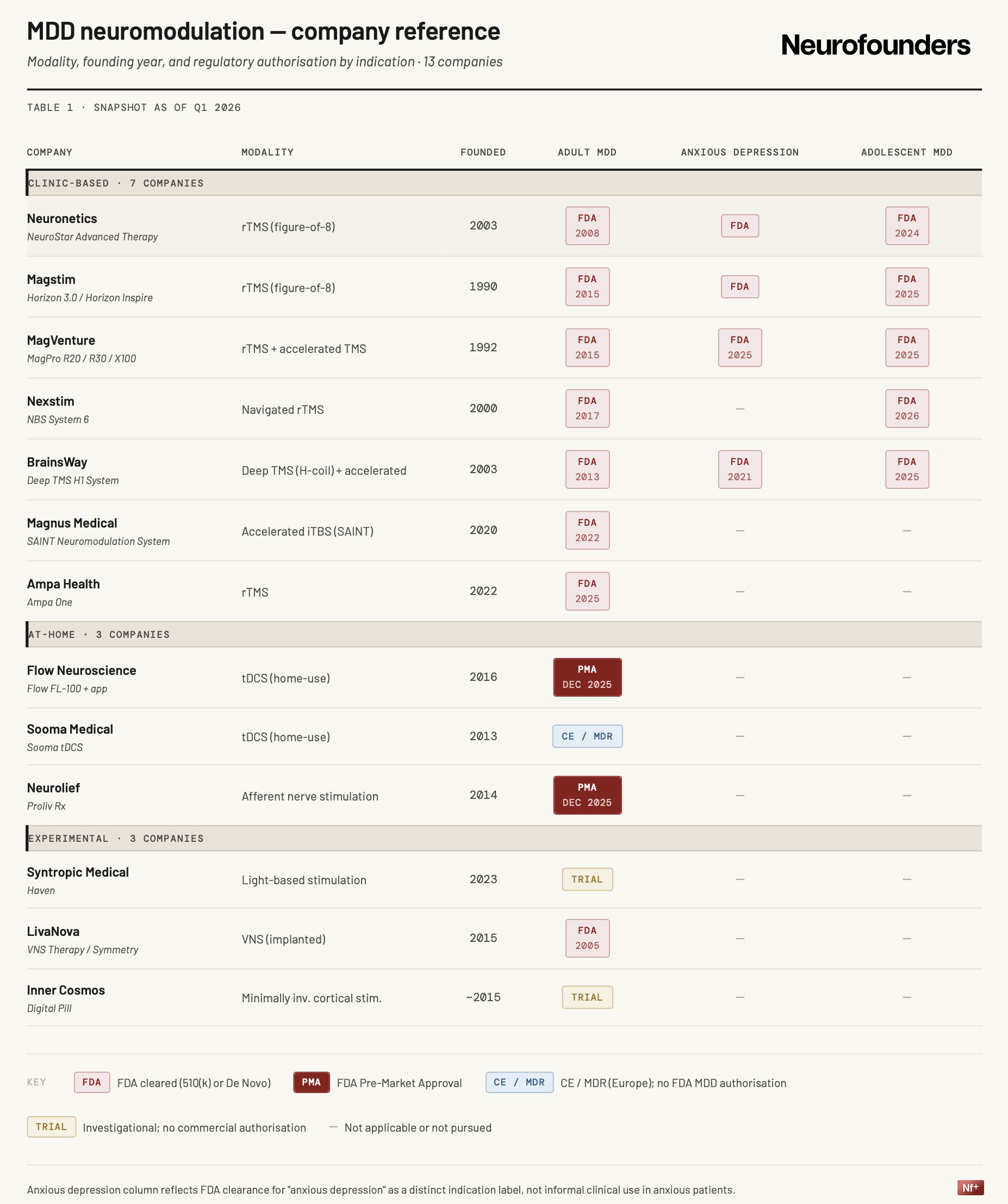

Adult MDD TMS is by now an established regulatory market. NeuroStar received FDA clearance in 2008, BrainsWay’s Deep TMS clearance followed in 2013. The current moment has surpassed basic validation into expansion across indications, protocols, and treatment settings.

That expansion is most visible in adolescent MDD. Neuronetics received clearance in March 2024, followed by Magstim in March 2025, MagVenture in August 2025, BrainsWay in November 2025, and Nexstim in March 2026. Prior adult clearance, combined with extensive safety records, make the label expansion an easy path to wider TMS availability.

Protocol is also becoming a more important competitive layer. Magnus Medical’s SAINT system was cleared in 2022 and entered commercial rollout in 2024. BrainsWay followed with FDA clearance for an accelerated Deep TMS protocol in September 2025. Speed, targeting, and workflow are starting to matter alongside the underlying modality.

The strongest recent regulatory signal came around the end of 2025. In December and January, Flow and Neurolief both received FDA PMA for depression-related use cases. The approvals differ in indication, modality, and positioning, but together mark the first real FDA opening for home-based neuromodulation in MDD.

The shift to at-home is also beginning to shape company strategy. BrainsWay’s successive equity investments in Neurolief following their PMA shows a direct move by a clinic-based TMS player into at-home mental health neuromodulation. It is an early sign that home use is being taken seriously not only by startups, but also by incumbents.

Outside TMS, experimental approaches are advancing, but remain early. Inner Cosmos represents the minimally invasive end of the spectrum, while Syntropic is exploring a non-invasive light-based route.

The snapshot still points to a market anchored in clinic-based TMS. But the layer around it is changing. TMS for adolescent MDD is expanding, accelerated treatment is becoming commercialized, while home-based neuromodulation has started to clear the FDA. The category is extending into new patient groups, new protocols, and new care settings.